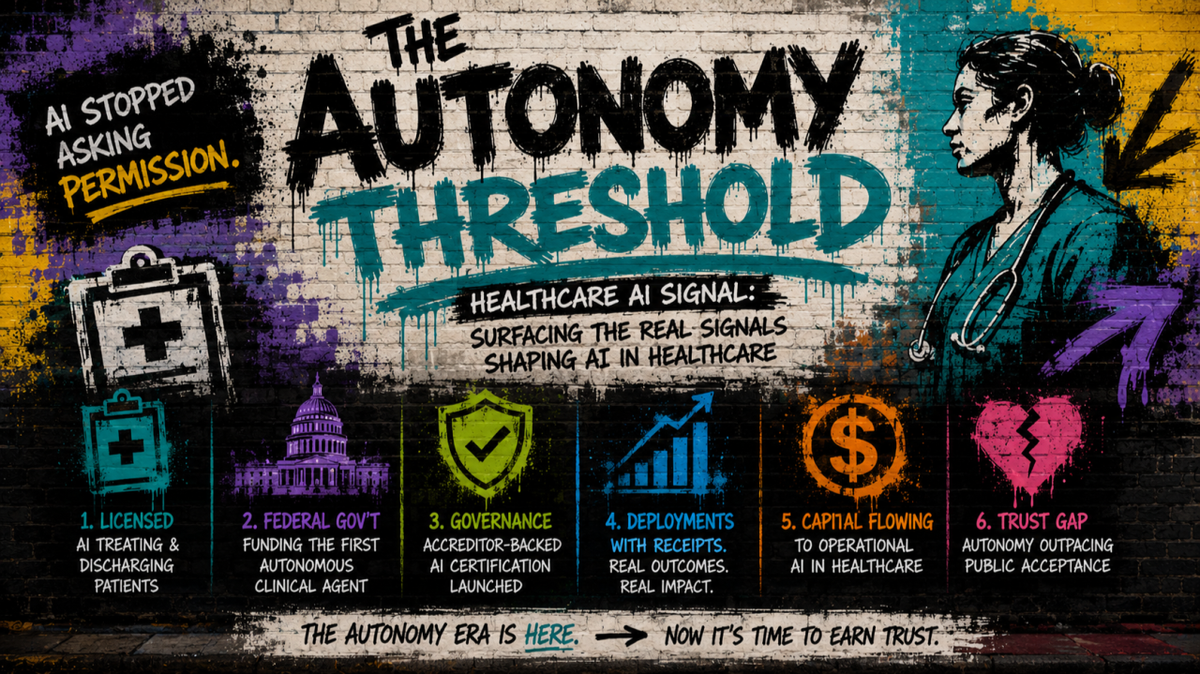

The Autonomy Threshold

Week of May 31 to June 6, 2026

This was the week AI stopped asking permission. In the span of a few days, the question shifted from whether AI can perform clinical work to whether institutions are ready to let it act on its own.

The clearest signal came from the UK, where Flok Health raised $12.5M to scale an AI physiotherapist that already holds regulatory clearance to triage, treat, and discharge NHS patients with no clinician in the loop. This is not decision support. It is a licensed autonomous operator working a defined pathway, and it moves the conversation from efficiency to liability. In parallel, the U.S. federal government moved to underwrite the same trajectory: ARPA-H's ADVOCATE program expects to name teams this month to build the first FDA-authorized agentic clinical-care system, putting public capital behind the riskiest part of the category, the regulatory pathway itself.

Governance raced to keep pace. The Joint Commission launched the first accreditor-backed AI certification, and Illinois passed the first state mandate for independent third-party AI audits. Both arrived faster than the sector expected.

1. Signal Summary

- Autonomy crossed from demo to license. An NHS-cleared AI physiotherapist that triages, treats, and discharges patients with no clinician in the loop raised a $12.5M Series A, the cleanest evidence yet of AI as a regulated clinical operator.

- The federal government moved to fund autonomy directly. ARPA-H's ADVOCATE program expects to name teams this month to build the first FDA-authorized agentic clinical-care system.

- Governance institutionalized, exactly as we predicted. The Joint Commission launched the first accreditor-backed AI certification (RUAIH), the move "Carrot and the Stick" forecast when CARF went first in April. We guessed 18 months; it took six weeks.

- Only the deployments with receipts made the cut. Optellum (250+ sites, 3M+ cases analyzed, FDA-cleared and Medicare-reimbursed) and Carbon Health (sub-4-minute notes, high provider acceptance) posted documented numbers. Several widely covered "deployments" announced activity without outcomes, and were left out.

- Capital concentrated on operational AI. Commure raised $70M at a $7B valuation; Lassie raised $35M for practice agents; PE poured record sums into RCM automation.

- The outlier: public acceptance remains soft (an April survey showed 42%, down from 52%). Autonomy is being licensed faster than trust is being earned.

2. Big Signal of the Week

Flok Health raises $12.5M to scale an AI physiotherapist the NHS lets work unsupervised

🔴 Major Signal | Score: 8.2 | View Article

Why It Matters Almost every "AI in healthcare" story is about a tool that helps a clinician. This is a tool that is the clinician for a defined pathway. Flok holds regulatory clearance that lets its AI triage, treat, and discharge NHS patients with no human in the loop, and it just raised institutional capital to scale it. The financing is not the story; the clearance is.

Key Details

- Organization: Flok Health, with investors AlbionVC (lead), Eka VC, Form Ventures, and Mercia Ventures

- Round: $12.5M Series A

- Clearances: Class IIa CE mark and CQC provider approval

- Capability: autonomous triage, treatment, and discharge of NHS patients with no clinician in the loop

- Status: live in production across multiple NHS areas

- Expansion: hip, knee, and pelvic-health pathways

- Specialty / domain: Orthopedics / patient access

What This Signals Healthcare AI is crossing from assistive tools into licensed, unsupervised clinical operators in defined pathways. That shift moves both labor allocation and liability, and it makes "which pathways can run autonomously" a real procurement question rather than a thought experiment.

My Read: The regulatory facts are doing all the work here, and that is exactly the point. Round size would be a weak signal on its own; standing Class IIa clearance to discharge a patient is not. This advances the autonomy thread we have tracked since "The Agent Threshold," but where Utah's Doctronic operated inside a state sandbox, Flok holds device clearance that travels. The question every operator should be asking is not whether this saves therapist time, but which of their own high-volume, protocol-driven pathways could be staffed by a licensed autonomous operator, and who signs for the liability when it errs. Watch for two things: comparable clearances in other pathways, and whether Flok publishes outcome and cost data from its live NHS sites. Clearance without outcomes is a moat. Clearance with outcomes is a market.

Source: The Next Web

3. Real-World Deployments

Optellum lung-cancer AI scales to 250+ sites with Medicare reimbursement

🟡 Real-World Deployment | Score: 7.8 | View Article

Why It Matters Reimbursement is the gate most clinical AI never clears. Optellum's lung-care platform is FDA-cleared, Medicare-reimbursed, and now running at scale across hundreds of sites with millions of cases behind it. That combination, payer alignment plus documented volume, is what turns a tool into a repeatable commercial model.

Key Details

- Organization: Optellum, with partners University of Pennsylvania Health System, Vanderbilt University Medical Center, and Bristol Myers Squibb

- Announced: June 4, 2026

- Scale: surpassed 250 clinical sites; over 3 million cases analyzed

- Products: Virtual Nodule Clinic and Lung Cancer Prediction AI, both FDA-cleared and Medicare-reimbursed

- Specialties: Radiology, Pulmonology, Oncology

What This Signals Oncology AI is moving out of pilots and into reimbursed, multi-site clinical workflows. Once a category has both clearance and a payment path, the procurement conversation flips from "should we evaluate this" to "why haven't we deployed it."

My Read: The number that matters is not 250 sites, it is the pairing of reimbursement with that scale. Plenty of AI tools can show a pilot site and a promising chart. Very few can show FDA clearance, a Medicare payment path, and 3 million cases of real-world volume at the same time. That trifecta is the difference between fundable and perpetually evaluated. The one thing missing is independent clinical or economic outcome data from the deployed sites; volume is necessary but not sufficient. If Optellum publishes that next, the lung-nodule category is effectively settled.

Source: PR Newswire / Optellum

Carbon Health rolls out hands-free ambient charting across all clinics

🟡 Real-World Deployment | Score: 7.2 | View Article

Why It Matters Ambient scribing is the most-hyped category in healthcare AI, and the most likely to stall at the pilot. Carbon Health pushed it across every clinic on its own EHR and reported a hard operational number: notes in under four minutes on average, with high provider acceptance. That is the achieved metric most ambient announcements never publish.

Key Details

- Organization: Carbon Health, with technology partners AWS (Transcribe Medical) and OpenAI

- Capability: ambient "hands-free" charting embedded in Carbon's proprietary EHR across all clinics

- Achieved metric: visit notes produced in under four minutes on average; high reported provider acceptance

- Domain / specialty: clinical documentation / primary care

- Note: company suggests the tool could become a commercial product

What This Signals Ambient documentation is shifting from pilots into repeatable operational deployments in outpatient settings. The category question is no longer whether the technology works.

My Read: The technology working was never really in doubt; what kills ambient deployments is what happens after. Recovered clinician minutes only show up in workforce metrics if they are deliberately reallocated, into patient time, reduced overtime, or different acuity ratios. Otherwise they dissolve back into the workload and nothing moves on the dashboard, which is the exact failure mode we flagged in "From Pilot to Practice." Carbon's sub-four-minute average is real and worth crediting. The follow-up question for any operator copying this is not "does it chart faster," but "what did we do with the time it gave back."

Source: Fierce Healthcare

4. Market Signals

NVIDIA, Foxconn and Taiwan medical centers bring agentic and physical AI to "Healthy Taiwan"

🟡 Market Signal | Score: 7.3 | View Article

Why It Matters This is AI moving off the screen and onto the hospital floor. A government-backed, roughly $1.5B program is putting agentic software and physical robots into named medical centers, including a nursing-collaborative robot, aimed directly at nursing labor and procedural workflows.

Key Details

- Organizations: NVIDIA and Foxconn, with Taichung Veterans General Hospital and Taipei Veterans General Hospital

- Systems: CoDoctor and NemoClaw (agentic AI) and Nurabot (nursing-collaborative robot)

- Program: government-backed "Healthy Taiwan" initiative, presented as a ~$1.5B effort; announced at GTC Taipei

- Use cases: ECG screening, AI-assisted colonoscopy, 3D cardiac reconstruction, and surgical planning

What This Signals Healthcare AI is advancing from narrow software tools toward integrated agentic and robotic layers. Operators will soon face multi-agent orchestration and hospital robotics as live infrastructure decisions, not distant experiments.

My Read: The interesting part is not any single robot, it is the stack: agents and physical hardware deployed together, under one national program, with NVIDIA positioned at the compute-and-orchestration layer beneath all of it. That is an infrastructure land grab, and it tells you who intends to collect the toll on agentic care. For U.S. systems, the read is to start scoping orchestration and robotics governance now, because the workforce implications land on nursing first. The missing piece is the same one as everywhere else this week: no measured time savings, error reduction, or staffing-impact data yet. Treat it as direction, not proof.

Source: NVIDIA Newsroom

NVIDIA survey: 70% of healthcare organizations now actively deploy AI

🟡 Market Signal | Score: 7.2 | View Article

Why It Matters The aggregate demand curve under every capital and deployment signal this week is now quantified: most healthcare organizations are not piloting AI anymore, they are running it.

Key Details

- Source: NVIDIA's second annual State of AI in Healthcare and Life Sciences survey

- Active deployment: 70% of respondents, up from 63% in 2024

- 85% of executives report AI is increasing revenue; 80% report cost reductions

- 46% plan AI budget increases exceeding 10%

What This Signals The industry has shifted from hype-driven experimentation to budgeted, in-production deployment. Budget intent is real and rising.

My Read: Useful as a temperature check, but read it with the source in mind. This is a vendor-sponsored survey, and the self-reported revenue and cost numbers will skew optimistic toward NVIDIA's ecosystem. The 70% deployment figure is the durable takeaway; the 85% "increasing revenue" claim is the one to validate against named-system data before quoting it in a board deck. The honest version of this signal is that budget intent is strong and adoption is broad, not that ROI is settled.

Source: NVIDIA

5. Policy and Regulation

Joint Commission launches the first responsible-AI certification for health systems

🟡 Policy / Regulation | Score: 7.6 | View Article

Why It Matters An accreditor most U.S. health systems already work with now has an AI standard. The Joint Commission's RUAIH certification turns "responsible AI" from a values statement into an auditable, organization-level framework.

Key Details

- Organizations: The Joint Commission, with the Coalition for Health AI (CHAI)

- Launched: June 1, 2026

- Scope: voluntary, organization-level certification covering governance, safeguards, monitoring, and education

- Focus areas: patient safety, quality, governance, privacy, and trust

- Important nuance: certifies the organization's AI practices, not individual AI products

What This Signals Healthcare AI governance is shifting from self-regulation toward standardized, accreditor-backed frameworks that will shape risk, trust, and procurement decisions.

My Read: This is the prediction landing. When CARF issued the first AI accreditation standard in April, I wrote that the Joint Commission, NCQA, and URAC would follow within 18 months. The Joint Commission followed in six weeks. For operators, the move is immediate: map your current AI controls against the RUAIH domains now and build the gap list before a payer, CMS, or a state references it in a contract. It is voluntary today with no enforcement teeth, which is exactly why early movers get to set the de facto bar. Governance is becoming the scale advantage, and the credential just became real.

Source: Becker's Hospital Review

State AI laws tighten on prior authorization, with Illinois adding a first-in-the-nation audit mandate

🟡 Policy / Regulation | Score: 7.4 | View Article

Why It Matters The state patchwork this newsletter has tracked for months is no longer abstract. Multiple states now constrain how AI can be used in prior authorization and claims, and Illinois added the first state requirement for independent third-party AI audits. Compliance cost is becoming a line item.

Key Details

- Washington SB 5395: prohibits insurers from relying solely on AI for prior-authorization denials

- Indiana HB 1271: restricts AI-only claim downcoding

- Maryland HB 1563: requires transparency reporting on AI use in adverse decisions

- Illinois SB 315 (View Article, Score: 7.2): pairs frontier-model safety with restrictions on AI in healthcare decisions and a first-in-the-nation independent third-party audit mandate; sent to Governor Pritzker, not yet signed

- Domain: revenue cycle and clinical decision support

What This Signals AI governance and audit features are becoming table stakes for market access, as state compliance burdens rise faster than federal rules.

My Read: Two patterns are converging. First, the human-in-the-loop mandate for payer-side AI is now spreading state by state, which means multi-state plans and the vendors selling to them need centralized compliance mapping, not workflow-by-workflow legal review. Second, Illinois just moved the bar from disclosure to audit, the first state to require an independent third party to examine the AI itself. That is a different order of obligation, and audit-readiness documentation is the thing to build now while it is still optional. The bill is unsigned and the healthcare provisions ride alongside broader frontier-model rules, so watch the Governor's signature and the final rule text for the enforcement specifics.

Source: Holland & Knight

6. Funding Signals

Commure raises $70M at a $7B valuation to run healthcare operations on AI

🟡 Funding Signal | Score: 7.6 | View Article

Why It Matters The market is now pricing operational AI as infrastructure. A $7B valuation for a platform that automates the back office, not a clinical breakthrough, tells you where capital believes the durable ROI is.

Key Details

- Organizations: Commure, with investors General Catalyst (lead) and Sequoia Capital

- Round: $70M at a $7B post-money valuation

- Scale: live in over 500 healthcare organizations

- Capability: automates over 85% of revenue-cycle work without human intervention

- Domain: revenue cycle management and clinical workflows

What This Signals Healthcare AI capital is concentrating around proven operational platforms that replace back-office labor at scale, rather than point solutions.

My Read: Back-office automation has the clearest ROI and the most motivated buyer in healthcare, and the valuation reflects that. When you evaluate RCM or workflow partners now, weight multi-site deployment evidence over feature lists; Commure's 500-org footprint is the kind of traction that justifies a platform multiple. The gap in the story is the same one that keeps recurring: the round and the valuation dominate the narrative, with no fresh published ROI or denial-rate data attached. The traction claim is credible. The outcome proof is the thing to ask for before you sign.

Source: Healthcare IT Today

Lassie nabs $35M to build AI agents for practices

🟡 Funding Signal | Score: 7.0 | View Article

Why It Matters Capital is flowing to agents that automate the administrative work crushing small and mid-size practices, the segment with the least capacity to build it themselves.

Key Details

- Organization: Lassie, with lead investor Andreessen Horowitz (a16z)

- Round: $35M Series A

- Scale: supports ~700 practices across 49 states; claims substantial labor savings

- Capability: AI agents that automate practice administrative work

- Domain: workforce / practice administration

What This Signals Accelerating capital allocation toward AI that automates routine healthcare operations is reshaping labor models in admin and revenue cycle, especially where staffing shortages are most acute.

My Read: The agent-for-practice-admin category is consolidating, and a 49-state, 700-practice footprint is a real distribution moat for a Series A. But the funding tracker frames it as a snapshot, not validated traction, so the labor-savings claim is still a claim. Pilot these tools, but hold them to customer-win and documented-outcome milestones before you bet a staffing model on them. The thesis is sound; the proof points are early.

Source: Fierce Healthcare

7. Research Breakthroughs

Insulet data backs Omnipod 6 and fully closed-loop automated insulin delivery

🟡 Research Breakthrough | Score: 7.6 | View Article

Why It Matters Diabetes care is moving toward devices that dose without a human deciding each step. Insulet's pivotal data pushes fully closed-loop automated insulin delivery from concept toward clearance.

Key Details

- Organization: Insulet

- Data: STRIVE pivotal trial and EVOLUTION 3 feasibility results, presented at ADA 2026

- Product: investigational Omnipod 6 with a fully closed-loop AID algorithm

- Finding: improvements in glucose control

- Status: pre-clearance; staged launch planned; IDE studies continuing toward regulatory clearance

- Specialty: Endocrinology

What This Signals The shift from hybrid to fully autonomous closed-loop systems in chronic-disease management is now near-term, raising expectations for algorithm-driven workflow ownership in diabetes care.

My Read: This belongs in the same week as Flok for a reason: it is autonomy in another guise, an algorithm taking over a continuous clinical decision rather than assisting one. The data is pivotal-grade, which is the credentialing step that moves a device from interesting to inevitable. The honest caveat is that it remains pre-clearance with no named health-system deployments yet, which is normal for this stage. Endocrinology leaders should stop building roadmaps that assume hybrid AID stays dominant, and start watching the IDE milestones and FDA interactions that will set the launch clock.

Source: MassDevice

Evidence over explanations: put medical AI to the test

🟡 Research Breakthrough | Score: 7.6 | View Article

Why It Matters The argument that should govern every AI procurement decision got published in a Nature-portfolio journal: demand proof that the model performs, not a story about why it decided.

Key Details

- Publication: npj Artificial Intelligence (Nature portfolio)

- Type: perspective article

- Core thesis: rigorous prospective performance evidence should drive adoption, not post-hoc explainability

- Specialties referenced: Radiology, Pathology

What This Signals Governance and procurement will increasingly demand prospective performance evidence instead of treating explainability as a proxy for safety or utility.

My Read: This sharpens the validation bar we have tracked since the Proof Era, and it lands a useful blow on a comfortable habit. "Explainable AI" has become a procurement security blanket: a model that can narrate its reasoning feels safe, even when no one has tested whether it actually performs. The piece says the quiet part out loud: an explanation is not evidence. The practical move for governance committees is to swap "is it explainable" for "show me the validation study design" in the vendor rubric. It is a perspective piece without new empirical data, so it is a frame, not a finding, but it is the right frame.

Source: Nature (npj Artificial Intelligence)

8. Trend to Watch

The week's signals line up on a single axis: autonomy is being granted faster than trust is being earned. Flok's unsupervised NHS clearance, ARPA-H's FDA-authorized agentic program, and NVIDIA's agentic-plus-physical hospital build in Taiwan all push toward AI that acts, not just advises.

Running underneath is the governance thread this briefing has followed for two months, and it reached a milestone. When CARF issued the first AI accreditation standard in April, I wrote that the Joint Commission, NCQA, and URAC would follow within 18 months. The Joint Commission followed in six weeks. Pair that with Illinois's first-in-the-nation third-party-audit mandate, and the accountability scaffolding is hardening faster than expected.

There's a quieter discipline in this week's deployment column, too. Of the dozen "deployments" that crossed the wire, only two (Optellum and Carbon Health) arrived with documented, achieved numbers. The rest announced activity. That gap is the signal: as "Cleared and Proven, but Not Yet Paid" argued, a deployment without published outcomes is still a pilot, no matter how it's framed. The tension between accelerating autonomy and hardening accountability is the defining dynamic of the next year, and the human signal (42% public acceptance) cuts against both.

9. Signal Scoreboard: Top 10

- Flok Health raises $12.5M for unsupervised NHS AI physio | 8.2 | Funding AI licensed to treat and discharge without a clinician.

- ARPA-H to select teams for FDA-authorized agentic clinical AI 8.0 Federal Government funding the first autonomous clinical agent.

- Optellum lung-cancer AI scales to 250+ sites | 7.8 | Deployment FDA-cleared, Medicare-reimbursed, 3M+ cases at 250+ sites.

- Commure raises $70M at $7B valuation | 7.6 | Funding Operational AI automating 85%+ of RCM work.

- Joint Commission launches RUAIH certification | 7.6 | Policy First accreditor-backed AI governance standard.

- Insulet backs fully closed-loop insulin delivery | 7.6 | Research Hybrid-to-fully-autonomous shift in diabetes care.

- Nature: evidence over explanations | 7.6 | Research Reframes procurement around validation.

- NVIDIA/Foxconn agentic + physical AI in Taiwan | 7.3 | Market Agents + robotics aimed at nursing and procedures.

- HSCC releases AI-specific cybersecurity governance guide | 7.3 | Governance AI risk becomes a distinct board-level discipline.

- Carbon Health deploys ambient charting across all clinics | 7.2 | Deployment Sub-four-minute notes with high provider acceptance.

10. Noise of the Week

Mayo Clinic and Microsoft join forces on a frontier health AI model

⚪ Noise | Score: 4.5 | View Article

Why It Looks Important Two of the most credible names in medicine and cloud AI, paired on a healthcare-specific "frontier" foundation model, with Mayo supplying and owning the clinical data and Microsoft providing the engineering.

Why It's Actually Noise It is a pure announcement: no development progress, no testing results, no workflow integration, no deployment. The model is only slated to be tested inside Mayo's own environment. The strategic logic (health systems treating proprietary data as an asset rather than becoming dependent customers of public models) is real, but there is nothing built yet to evaluate. The brand wattage is doing all the work.

Source: TechTarget (HealthTech Analytics)

Athenahealth rolls out 80+ new and expanded AI RCM features

⚪ Noise | Score: 4.8 | View Article

Why It Looks Important A major EHR vendor and a big number: 80-plus new AI features across athenaOne RCM, from automated insurance selection and AI copay to voice AI, express coding, and denial-resolution automation.

Why It's Actually Noise It is feature-counting with no named deployments, no adoption data, and no outcomes. Until customers report reductions in denial rates or days in A/R, this is a roadmap, not a result, the same standard that kept four metric-less "deployments" out of this issue. Thats the purpose of this newsletter, to count the outcomes, not the features.

Source: Fierce Healthcare

11. Executive Takeaway

If this becomes a trend then the proof era graduated this week into the autonomy era. The strategic question is no longer "does AI work" but "where am I willing to let AI act on its own, and is my governance ready before the regulator's is?" The Joint Commission moved three times faster than we forecast. Build the accountability scaffolding now, while it is still an advantage rather than a scramble. And hold every "deployment" to the Optellum/Carbon Health bar: if it doesn't come with an achieved number, it's still a pilot.

Healthcare AI Signal is a high-signal (no-noise) briefing on the developments actually shaping AI in healthcare. Its lens is inspired by street art: honest, urgent, and grounded in what is really happening, not just what official narratives choose to highlight.